If I had my way, I would write the word "insure" upon the door of every cottage and upon the blotting book of every public man, because I am convinced, for sacrifices so small, families and estates can be protected against catastrophes which would otherwise smash them up forever.It is the duty to arrest the ghastly waste, not merely of human happiness, but national health and strength, which follows when, through the death of the breadwinner, the frail boat in which the family are embarked, founders and the women and children and the estates are left to struggle in the dark waters of a friendless world.

Winston Churchill

The actuaries' crystal ball

Many novelists and philosophers have considered what it would be like to be able to see into the future. Would you dare to look? What effect would it have on you if you discovered that tragedy lay ahead? What would you do differently in your life if you could see your future in a crystal ball?

Detail from "Allies" by Lawrence Holofcener showing Winston Churchill and Franklin D. Roosevelt talking on a park bench, New Bond Street, London

It is precisely because none of us can predict our futures individually that it is so important for us to attempt to predict them collectively. In the quote above, Winston Churchill expresses very eloquently the importance of insuring ourselves - with pensions and life assurance, for example - against destitution; but in order for governments, employers, and financial institutions to arrange such insurance, they must have some idea of the future cost of commitments they make in the present. So they employ actuaries, whose professional motto is "making financial sense of the future", to look into their crystal balls and see what is in store.

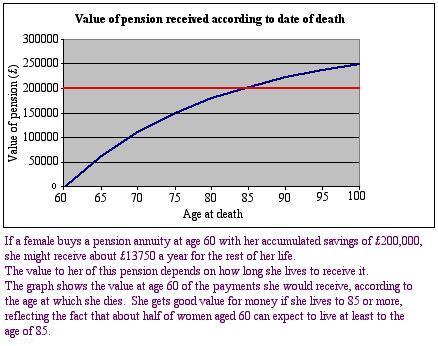

Take pensions, for example. Although most people think of private pensions simply as savings and state pensions simply as benefits, there is also an important element of insurance in a pension. Technically, a pension insures you against so-called "longevity risk", which is the risk that you will live longer than expected. This isn't normally thought of as a risk, but suppose for a moment that, instead of arranging a pension during your working life, you just put some money aside each year, intending to live off that when you get old. How much should you put aside? You could assume that you will live an average life - but some people live decades longer than average, so you would risk running out of money. But putting aside enough to live on till 120 will (sadly) almost certainly be unnecessary - and very expensive indeed. So governments, employers and private pension providers must make complex actuarial predictions in order to afford the pension promises they make.

A pension can come from one of two places - money put aside while the pensioner was in work, a system known as "funded"; or taxes paid by people currently in work, known as "pay as you go". Calculating the amounts that need to be saved in pension funds, or "transferred" between the young and the old, and the promises that can be made about future payouts, is an enormous exercise in financial modelling, for governments, employers, pension funds and financial institutions. Noone knows more about this complex subject than the Government Actuary, Chris Daykin, so Plus went to talk to him at the Government Actuary's Department in London.

The Pensions Crisis

I'll be paying how much tax?

Image DHD Photo Gallery

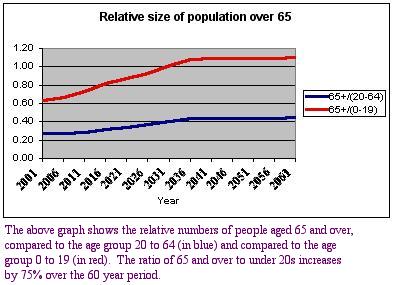

Much has been made recently in the financial pages of the popular press of a so-called "pensions crisis". According to Daykin, different people mean different things by this phrase. "Internationally, people talk about the pensions crisis because of the ageing population", he says. "There's an imbalance, with people paying contributions during their working lifetime to finance the pensions of people who are elderly at that time. In the future there will be far fewer people working, relative to the number of people receiving pensions. So that would make it very expensive to go on paying pensions at the same sort of level."

The situation is rapidly becoming desperate in countries such as Germany and Italy, where state pensions have been quite generous and birth rates have become very low. Demographers can see that in another couple of decades, there will be so many older people, to whom generous promises are being made, that young people will have to pay as enormous proportion of their income in tax to keep these promises.

In the UK, something slightly different is meant by the phrase "pensions crisis". Daykin says that "governments have very carefully taken account of the longterm consequences when making pension promises, and therefore the pension promises are more restricted in the UK than in other countries." But before you breathe a sigh of relief, there's something you should know: "Our crisis is more at the other end - are people going to have enough pension to live on, particularly pension from the state? People are expected to be making their own arrangements for their pension through occupational schemes and personal pensions, but a lot of people don't get round to it or opt out of such schemes."

A colossal balancing act

The job of the Government Actuary's Department

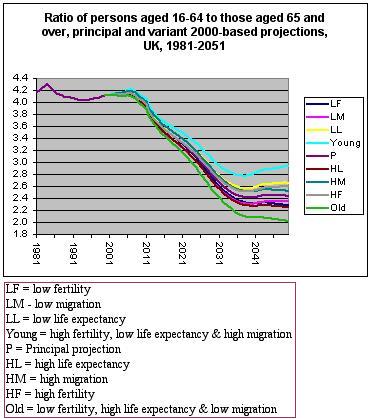

Whichever way is chosen - funded, or pay as you go - providing pensions is really a colossal balancing act. Firstly, pension promises have to be pitched at a level high enough to protect pensioners against poverty; secondly, the money has to be found to keep those promises. Decisions must be made today about events in the far future; events which depend on such things as changes in life expectancy and health, emigration and immigration, the economic cycle, future employment rates and birth rates... the list goes on.

The Government Actuary's Department is charged with carrying out this balancing act for the government. It models the cost of pensions systems and provides advice on the future consequences of particular policies. It also gets involved in the formulation of policy, advising government on what will work, the interaction between the public pension system and private pensions, what private pension schemes can and will do, and so on. According to Daykin, "a lot of it is about judgment calls."

Daykin explains that his department's predictions are made using multistate modelling. "There are a number of states people can be in - working, retired, retired on ill health, dead but having a survivor - and each of those has a benefit or a contribution associated with it which can then be modelled into the future, with a variety of assumptions about the probabilities of different events. It depends very much on the purpose for which it is to be used but certainly there's no single answer. We're looking for some sort of best estimate, and then alternative scenarios or a range about that.

"For most purposes we're not using fully stochastic models because we don't know enough about the relationships between the different variables. A stochastic model would be one which operates on statistical principles - that generates probabilities of events in future years from distributions using some random number generation process. But it is quite difficult to get robust models which you

are confident will actually represent what will happen in the future. So it's more common in this type of modelling work to use a variety of different scenarios - to make a number of assumptions that give you a range of possible outcomes, but where it's not necessarily possible to ascribe a probability to each outcome."

The actuaries' crystal ball

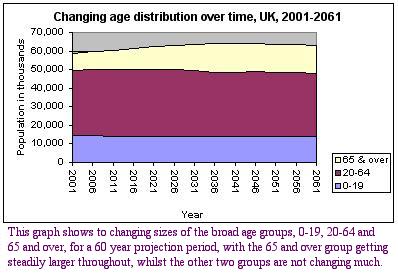

Daykin gives an example of the sort of difficulty that can arise. "Every year the Office of National Statistics move forward their estimate of the population based on the previous census, numbers of births and deaths registered, an estimate of migration based on surveys taken at ports and airports - and those estimates, once you get ten years down the line from the last census, have inevitably wandered off a bit. And we're using those as our base to project forward sixty years into the future!" The most recent census was in 2001, and when the results were released at the end of 2002, it turned out that the UK population was about a million lower than had been predicted. Clearly, a discrepancy of this magnitude has serious implications for the models on which the government's predictions of future pension costs depend, and it has been quite a headache for the Government Actuary's Department. As Daykin says, "it is a bit scary that even the baseline is a bit wobbly."

However, he is quite philosophical about the situation. "One of the lessons one learns in projecting the future is that you have to keep on updating your estimates; you can't just sit back and see what happens. You're constantly getting new information, which is then used to feed back into the assumption-setting process, and in some cases into the modelling process itself. And then the policy-making process has to take into account this uncertainty. It should be robust - you can't base policy on one specific outcome."

There's feedback in the system

Not only is there uncertainty about the information on which models and predictions are based, but policies themselves feed back into the decisions people make. He gives an example. "If you change the rules about pensions in any way, it makes people take different decisions," says Daykin. "It may change the way in which employers deal with early retirement cases. The definitions of when people are perceived to be disabled or ill enough not to work change quite radically over time, depending on the employment situation.

"Those sorts of things are very difficult to predict. There are things you know will have an impact but you don't know quite how to quantify it - for example, when you introduce flexibility in retirement age it will undoubtedly have an impact on people's working habits. And in order to make your projections you have to make some assumptions about how people are going to respond to that, monitor what actually happens, and change those assumptions as the situation develops."

Advice - accepted and ignored

Who makes the decisions in the end? Daykin is clear on this: "Having once advised, we don't make decisions - governments make decisions. Our aim is to explain what the consequences of a policy will be - not to prevent governments from doing what they want to do - and then explore the consequences in a way which will help governments to make good decisions."

The pension mis-selling fiasco - wealth destroyed.

Image DHD Photo Gallery

Has he ever been frustrated by having his advice ignored? "There was a high-profile occasion in the mid-80's, when the Conservative Government was keen to free up choice in pensions, and they wanted individuals to be able to choose whether they belonged to occupational pensions or not, and to have the right to take out personal pensions. One of the things they wanted to do was to say that it would be made illegal for an employer to insist on an employee belonging to a pension fund. That was a policy decision, and our advice was that this would lead to chaos, because it would make it very difficult for individuals to know what they should do - they would become prime targets for insurance companies to sell possibly inappropriate pensions products to, particularly as at the same time the opportunity was being given to people to opt out of the state scheme as well. So individuals could both increase their takehome pay, by paying lower contributions to their employer's pension scheme, and also take out a pension scheme and think they were doing fine, and be told that they were getting a potential benefit, but actually be losing out on all the contributions that the employer would normally have put into the pension scheme for them.

"That was the start of the pension mis-selling fiasco, which has really undermined the whole financial services industry and people's confidence in pensions generally. Insurance companies, following their natural tendencies, went out to sell a lot of this business. Here was a huge new market for them. They were encouraged to do so. The government put advertisements in national newspapers saying personal pensions are now available.

"It was very frustrating, because we told them what would happen and it did."

A word from the wise

The earlier you start, the cheaper it is

What single bit of advice would Daykin give to young people today? "I think they should know that the state is not likely to provide them with a very high level of income in retirement. They should certainly be aware that they need to make their own pension provision. That's not to say that they should necessarily start doing it straight away, although in some ways the earlier you start doing it the cheaper it is. The power of compound interest is quite strong.

"It's difficult to say to young people that they need to be putting a lot of money away when they're young, but they need to be thinking about their lifestyle and their financial needs over their working lives, and not leaving it too late, because if you wait until you've sorted out these other things and you're 40, retirement is coming close in terms of being able to provide for it."

Don't say you weren't warned...